The bond market is about to enter a phase we haven’t seen in over 70 years…

A rising interest rate cycle.

A trend that has only been accentuated by the Federal Reserve’s aggressive plans to accelerate interest rate hikes and ongoing concerns over an impending major stock market correction.

And while it is too early to jump on the “Death of the Bond Bull Market” sentiment swirling around Wall Street, the current direction of interest rates could be worrisome for U.S. oil producers.

You see, any way you look at it, a wide swath of U.S. oil and natural gas producers are going to take rising rates on the chin. Bankruptcies, mergers and acquisitions, and asset sales one step ahead of the sheriff will be increasing.

That doesn’t mean there’s no profit to be made here… On the contrary, in fact.

Those are all opportunities.

But it does mean we may have to tread carefully…

How the Fed Could Hammer U.S. Oil Producers

The current collision between Fed interest policy and U.S. oil and gas operators reminds me of a problem that first started to appear in late 2014.

At that time, the collapse in oil prices was underway, and one of the pervasive elements of U.S. oil producers was first revealed…

Virtually all U.S. publicly traded or privately held oil and gas producers are “cash poor.”

That means the companies rely on debt to cover the bulk of near-term operating costs. Proceeds from sales are (more often than not) employed to cover dividends or stock buybacks. In fact, if left only to the revenue derived from sales, many producers would go belly-up rather quickly.

As a result, they resort to taking out credit.

Now, this is not as strange as it may seem.

In fact, for most producers, this was a very manageable arrangement.

But it does have a downside if the situation becomes more constricted…

The Problem With Energy Debt

The ability to use oil that hasn’t been drilled yet as collateral for a line of credit becomes problematic once the price that oil can command declines significantly.

Furthermore, as oil and natural gas prices decline (and the ability to obtain new credit is restricted), the high-yield energy curve rises faster than any other bond sector. Related: The U.S. Oil Industry Sets Its Sights On Asia

Which is precisely what began in earnest at the end of 2014.

2012-2014 spread of high yield energy bond rates to high yield rates; lhs = “left-hand side,” the bid or buy price. Source ASIDA analysis

You see, as the spread intensified, it put downward pressure on U.S. producers.

For example, as oil prices started to fall in 2014 after OPEC opted not to cut production, equity values for publicly traded American companies declined as well.

But the overall affordability of available credit declined even faster.

Source: ASIDA analysis

The result was the largest bankruptcy spike in decades.

Which brings us back to the situation developing currently…

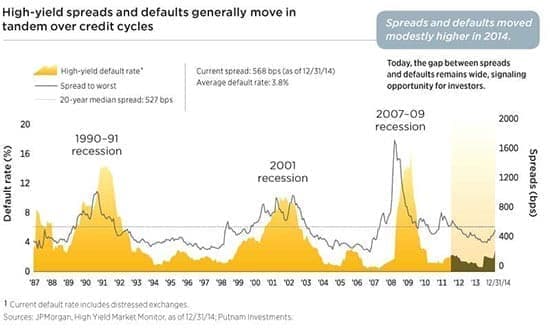

You see, there is a historical connection between a widening yield spread and company defaults.

In fact, as you can see in the chart below, these two have moved in tandem with each other for decades…

Now, some analysts believe that the situation we’re seeing today won’t be as bad as what we saw back in 2014-2016.

And there are three predominant reasons why…

1. Oil prices are some $20 a barrel higher;

2. Operations have become more efficient;

3. And a balance is forming between supply and demand.

But if you take a closer look at the situation, none of those reasons are all that positive…

2014 Vs. 2018

To start, even though the West Texas Intermediate (WTI) oil price is currently at $62 a barrel, what the operator receives is much less.

It’s called the wellhead price, the first arms-length transaction in the field between producer and wholesaler.

That tells a very different story.

Despite higher prices, most operators are once again in breakeven territory…

The key here is the number of “half-cycle” fields available for further production.

Half-Cycle: mature fields with all common cap ex; Cumulative Reserves: remaining to produce plus undiscovered resources; Discount: wellhead price to WTI

Even at current prices, it remains a losing proposition for most operators to commit capex to opening new “full-cycle” projects (and their associated infrastructure expenses).

Meaning that higher oil prices are simply not enough.

Which brings us back to the situation developing currently…

You see, there is a historical connection between a widening yield spread and company defaults. Related: What Is The Right Price For Oil In A Balanced Market?

In fact, as you can see in the chart below, these two have moved in tandem with each other for decades…

Which brings us to the second point: increasing efficiency.

From the onset of the OPEC-induced downward pricing cycle, U.S. producers found ways to cut costs by at least 17% across-the-board.

That helped somewhat… but it also had a declining advantage.

Most of the savings were passed upstream in the cutting of costs charged by oilfield service (OFS) providers.

That has ended with the renewal of increasing drilling and rising OFS charges.

In addition, cutting corners on supplementary expenses has bought some time, but deferred maintenance on infrastructure has also pushed forward bills that now are coming due.

Meaning those elements contributing to increasing efficiency in operations are not available this time around.

All while the costs of doing business are rising.

Finally, we have the balance between supply and demand.

While the combination of increasing U.S. exports and the deepening problems in certain OPEC producing nations (e.g., Venezuela, Nigeria, and Libya) has allowed for an increase in overall volume from U.S. companies, the expected rise of aggregate production to well above 10 million barrels a day will begin to put pressure on oil prices.

While this is not likely to result in any pronounced selloff, it also will not be able to absorb the expected further rise in domestic volume.

Fact is, what makes this impending rise in high yield energy bond rates so different from what transpired in 2014-2016 is the source.

This one is emerging from a direction in the broader bond market pressures.

Given the disposition of the Fed and the attitude of investors, this one is likely to be longer-term.

While manageable, I am now expecting another round of debt problems for some producers.

But on the flipside, this sort of pressure always provides some nice investment opportunities in both the insolvency and M&A markets.

And you can rest assured that I’ll be keeping you updated as those investment opportunities arise.

By Dr. Kent Moors

More Top Reads From Oilprice.com:

- Saudis Ready To Swing Oil Market Into Deficit

- Has OPEC Been Too Successful?

- Tech Giants Scramble To Secure Cobalt Supply