Via MetalMiner.com

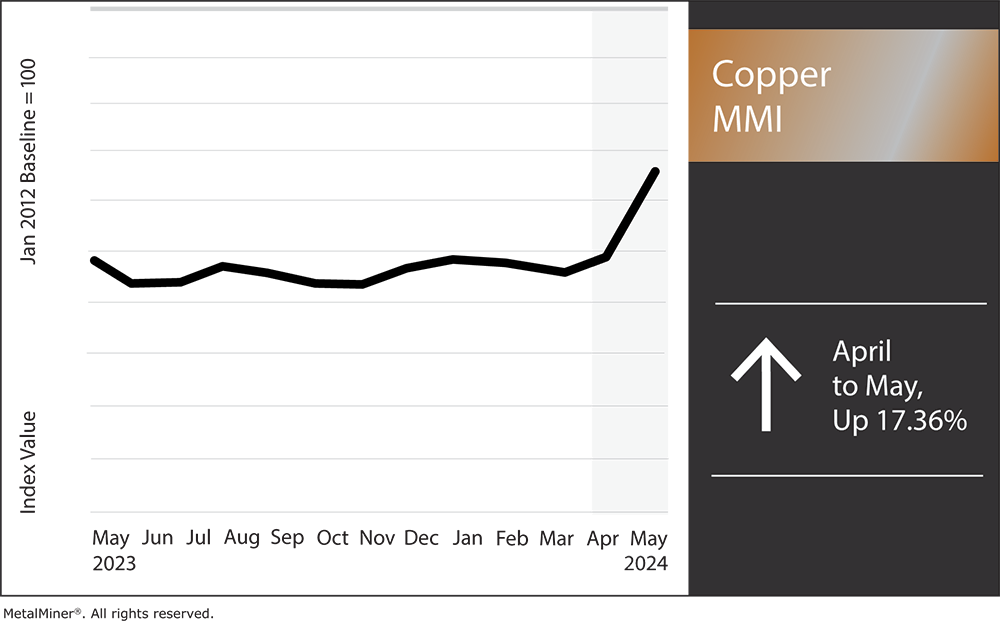

Overall, the Copper Monthly Metals Index (MMI) rose 17.36% from April to May.

The copper price uptrend accelerated throughout April. Bullish momentum saw prices surge nearly 14% from the close of March. By April 29, prices pushed past the $10,000 per metric ton mark. They continued to move even higher by mid-May, with an additional 1.14% increase. Despite these recent surges, the copper price today still faces numerous risks.

Long-Term Fundamentals Drive Copper Pricing Above $10k Per Metric Ton

Unstoppable copper? If you ask a copper bull, nothing can get in the way of the current uptrend. Long-term market fundamentals go as follows: tight mine supply and the lack of investment in new mines, growing demand from sectors like renewables, grid investment, and war, plus the need for AI-driven data centers means copper prices are on a one-way journey north.

From a long-term perspective, supply concerns remain valid. Mine disruptions and closures, combined with increasingly lower ore grades from operating mines, have already translated into plummeting treatment and refining charges. While higher copper prices will likely trigger the development of new mines, it takes an average of 16-17 years from discovery to production. Therefore, outside recycling, boosting the supply pipeline cannot happen immediately, even with proper investment. Meanwhile, an increasingly electrified world means the demand for copper will grow. This is the main reason for the current copper supply deficit forecasts, which expect shortages to start in 2025.

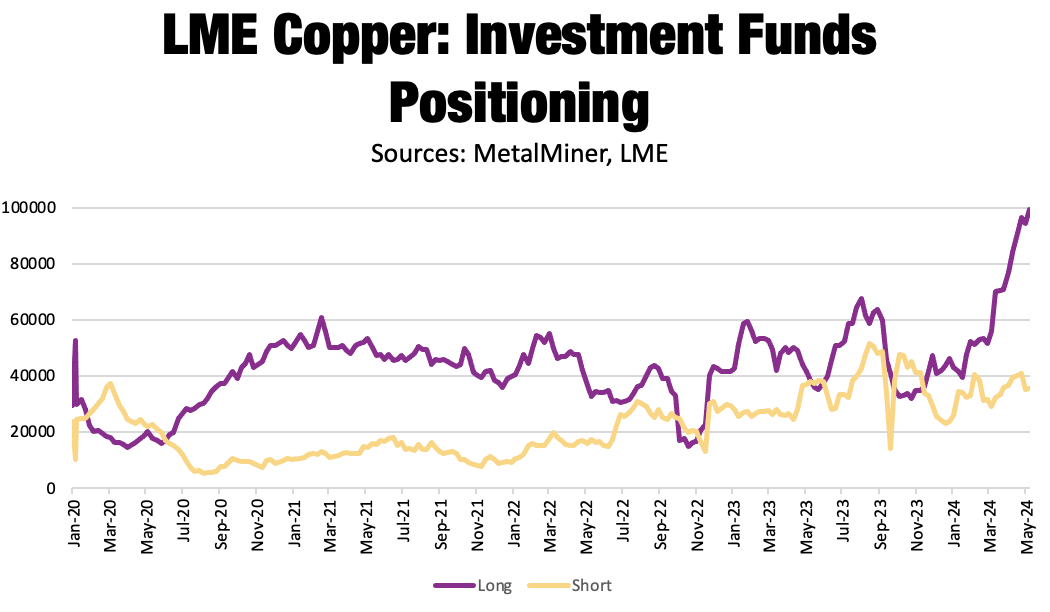

The LME investment fund spread appears decisive. By early May, long positions represented nearly 73% of total investment fund positions. While total short positions remained relatively stable, bets on higher copper prices more than doubled since early January. The substantial rise in long positions helped copper prices hit their highest level since April 2022 by mid-May.

Meanwhile, CME prices appeared even more bullish. On May 14, a copper squeeze caused intraday trading to temporarily climb above the $11k per metric ton mark. While prices reeled back by closing, CME prices closed May 14 at a more than $300/mt premium above LME prices.

Speculative Bets Fuel Too Far, Too Fast Concerns

Ahead of the current rally, an upcoming bull trend for copper prices was possibly the worst-kept secret in metal markets. After all, copper remains essential to the global green transition currently underway. This fact alone left many market participants ready to pull the trigger on long bets as soon as copper prices began to rise.

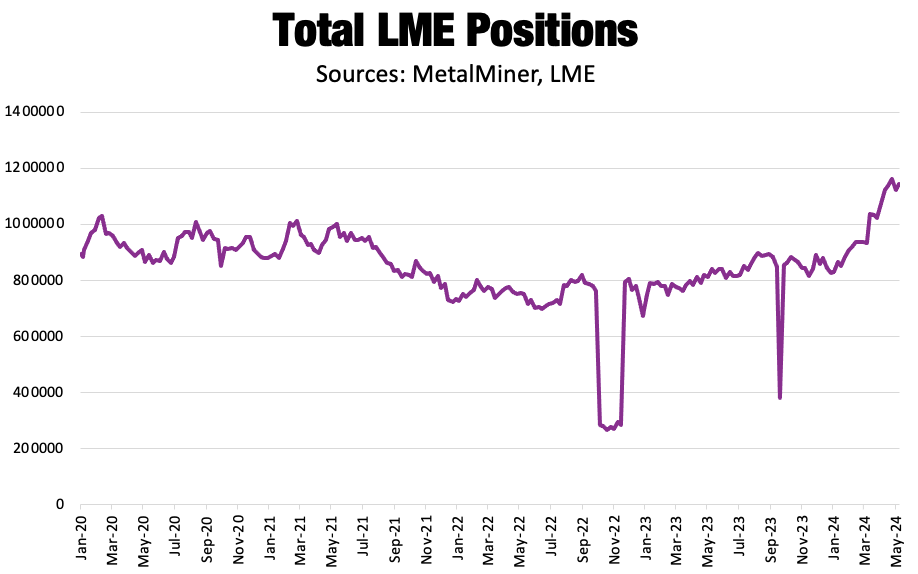

The start of 2024 seemed to spark new interest in metal trading overall. Likely aided by the Russian aluminum, copper, and nickel trading ban imposed by the U.S. and UK, LME trading volumes hit an all-time high during April, with over 17 million contracts traded. For copper, the total number of positions on the LME saw a more than 38% increase from the close of 2023 to May 10. And the LME was not alone, as both the CME and SHFE also saw increased market participation.

The renewed boom in trading offered momentum to all base metal prices. Irrespective of current supply conditions, these continue to trade up from the start of the year. However, with the wave of speculative bets comes a significant risk that demand may not keep up with expectations. This is, in fact, one of the main issues haunting copper prices today.

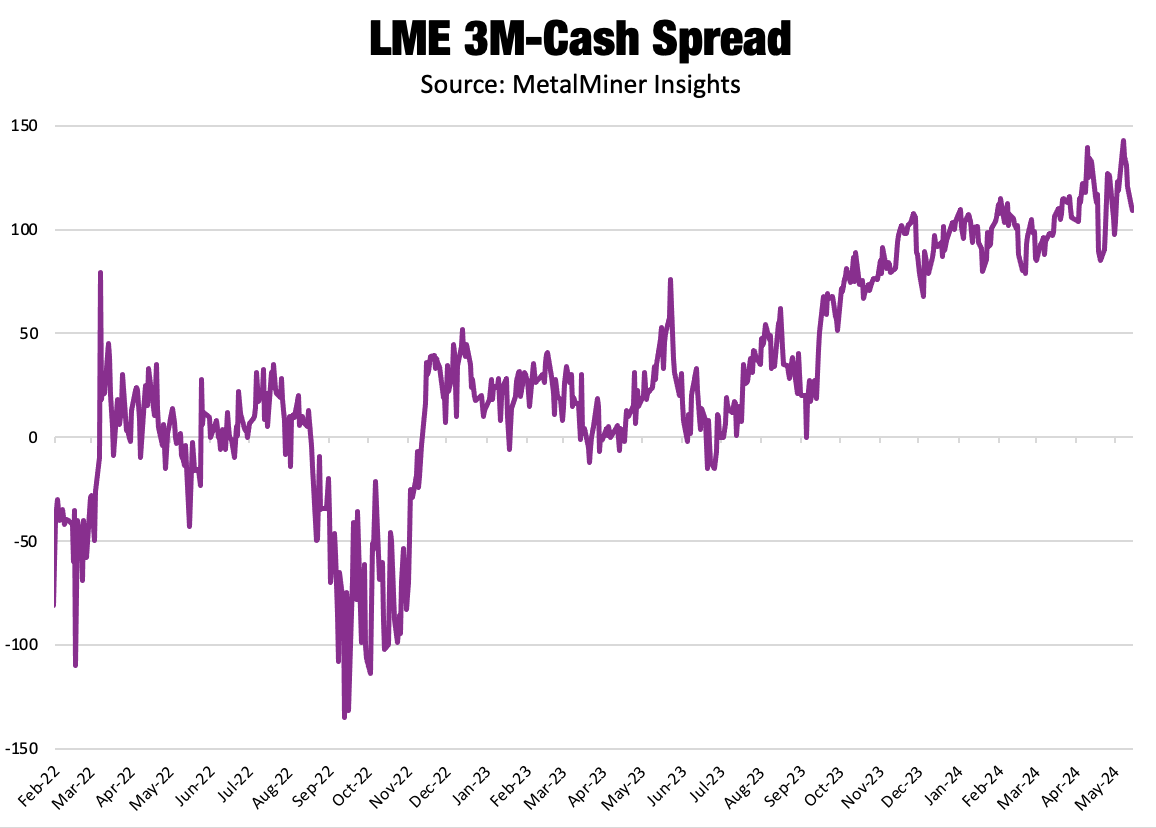

Longstanding demand signals remain a nagging red flag to the current reality of the market. For one, the deeply entrenched contango between LME three-month futures and primary cash prices suggests a well-supplied market. By May, the futures premium hit an all-time high of $143/mt. While it retraced slightly during the following week, the average premium since 2012 pales in comparison at just over $12/mt.

Copper Price Today: Chinese Demand and Green Energy Suffering

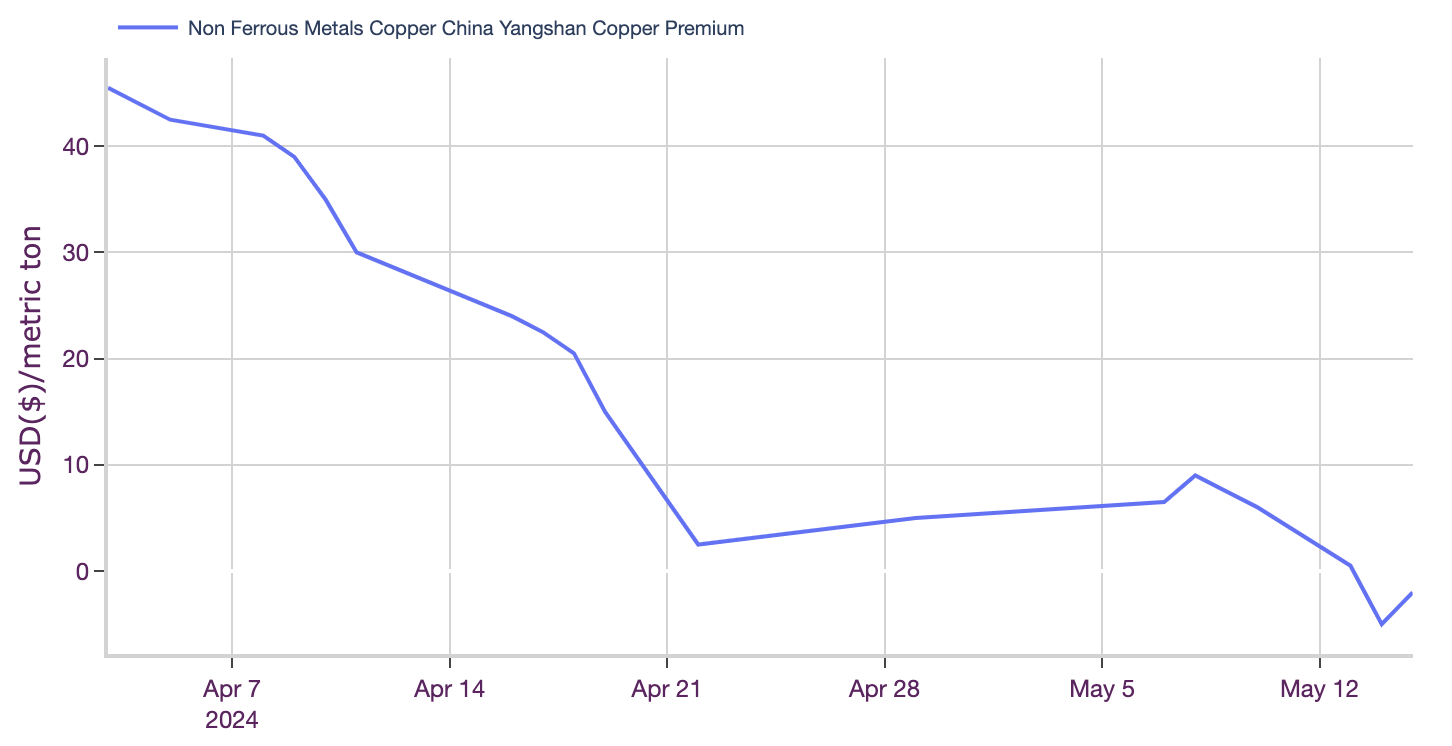

Meanwhile, demand indicators in China are also not living up to the current hype. China’s Yangshan copper premium dropped below zero by mid-May, as if to indicate that higher copper prices put a lid on demand. It’s also not hard to imagine that higher metal prices could squelch demand in the U.S. sectors like offshore wind and EVs continue to face setbacks because of costs and profitability, and spiking copper prices leave sectors that require a considerable amount of copper vulnerable.

While the long-term bullish market fundamentals remain valid, it’s difficult to ascertain how long speculation can carry the market, especially as fear of missing out on the current trend pushes prices unsustainably high. Should large position holders begin to unravel those bets, a downside correction could be looming in the shadows.

Copper Market Unknowns

Amid the current market volatility, there are many lingering unknowns that could impact market conditions. Although inflation cooled in April, it remains higher than the Fed’s 2% target. Moreover, the Federal Reserve has yet to indicate a timeline for rate cuts and will likely require sustained progress on inflation before officials are ready to pivot. Spiking metal prices certainly will not help the Fed’s ambitions. Meanwhile, higher-for-longer interest rates will continue to support the U.S. dollar. As copper prices move inversely to the U.S. dollar index, this will continue to temper demand.

In other news, May saw Panama elect a new conservative president, who promised to help pull the economy out of its current slump. The copper market also saw a significant impact from the closure of First Quantum’s Cobré Panama copper mine, which accounts for an estimated 1% of global copper supply. Triggered by environmental protests, the mine closure worsened ore supply tightness for copper smelters. However, Panama’s government agreed on a new contract with First Quantum to resume concentrate processing operations by early May.

Days earlier, the new president, Raul Mulino, left markets with optimism that First Quantum could renegotiate a new contract to resume mining operations. Mulino told a Panamanian radio show, “To even consider the mining issue, the arbitration has to be suspended.” First Quantum initiated arbitration proceedings following the mine closure, seeking compensation of $20 billion from the country. While resuming mining operations would likely also require a new contract that is more favorable to the Central American nation, it leaves the door open that Cobré Panama is not yet closed for good, which could help ease current supply concerns.

Biggest Moves in the Price of Copper

- Indian primary cash copper prices saw the largest overall increase, with a 14.23% increase to $10.40 per kilogram as of May 1.

- Chinese copper wire prices remained bullish, rising 13.22% to $10,071 per metric ton.

- U.S. copper producer prices for grades 110 and 122 rose 11.64% to $5.66 per pound.

- U.S. copper producer prices for grade 102 rose 11.09% to $5.91 per pound.

- Korean copper strip prices saw the only, albeit modest, decline of the index. Prices edged lower, dropping 0.23% to $10.28 per kilogram.

By Nicole Bastin via AgMetalminer.com

More Top Reads From Oilprice.com:

- Consumers Sue U.S. Shale Alleging Collusion to Boost Oil Prices

- Europe Needs To Address Intermittent Renewables Generation

- The IEA Has Cut Its Oil Demand Growth Forecast for 2024