Via Metal Miner

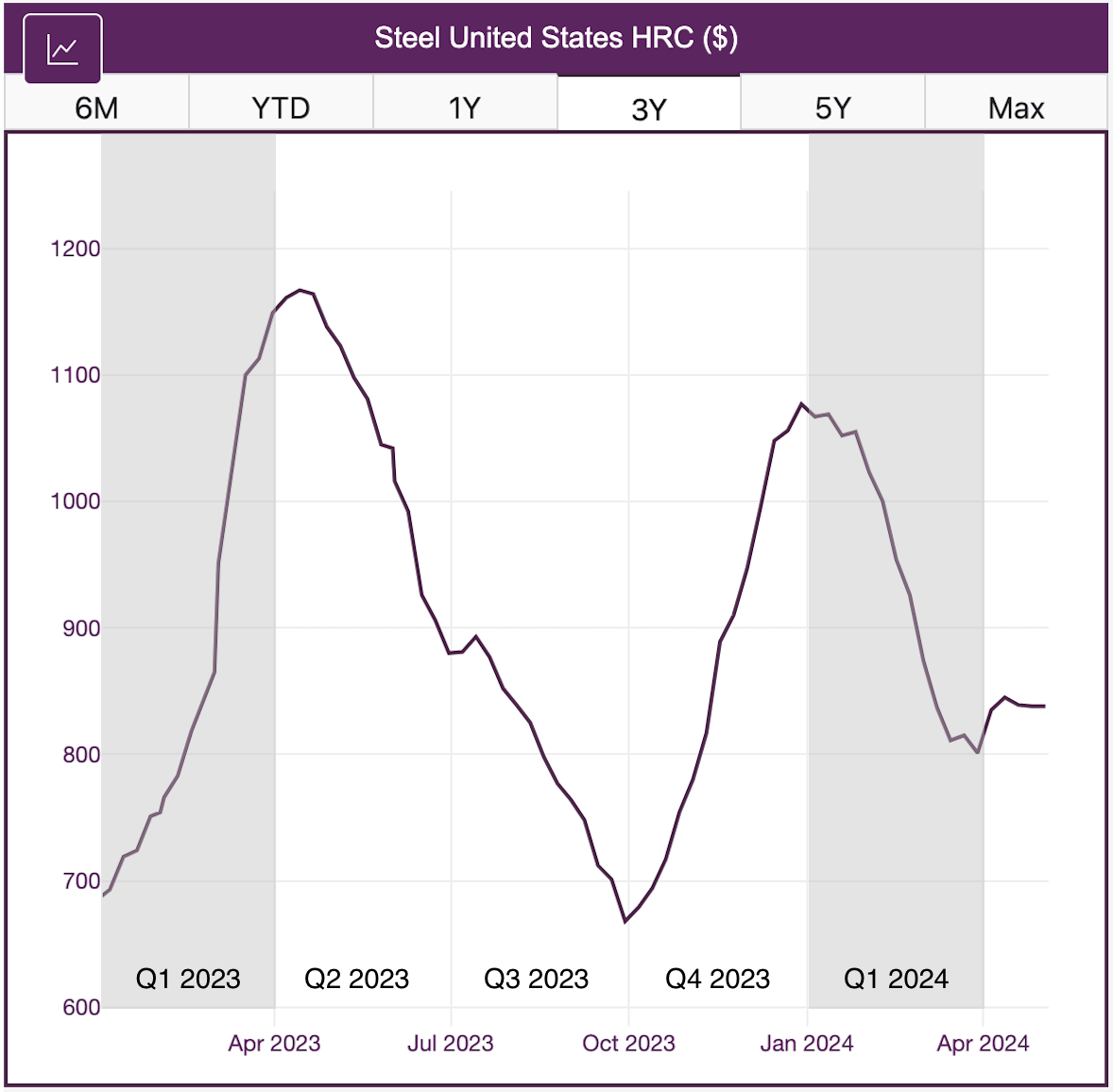

The Raw Steels Monthly Metals Index (MMI) moved sideways, with a modest 1.86% decline from April to May. U.S. flat-rolled steel prices found a bottom at the close of March and proceeded to move sideways. HRC prices saw a modest increase but ultimately closed the month at $838 per short ton. Meanwhile, HRC Midwest Futures saw a strong decline throughout April, which saw the delta between MetalMiner HRC prices and futures narrow to a mere $1 per short ton as of May 1. This signals that markets expect the sideways steel price trend to continue near current levels.

Nucor, Cliffs Publish Weekly HRC Prices

Two major steelmakers recently announced new initiatives to publish HRC spot prices. Nucor led the market, publishing weekly prices on Monday, April 8. Cleveland-Cliffs followed Nucor, releasing a monthly “Cliffs Hot Rolled Market Price” on Friday, April 26. According to reports from World Steel Dynamics, Steel Dynamics (SDI) does not intend to follow moves by Nucor or Cliffs.

By Friday, May 3, Nucor’s price stood at $825 per short ton, while Cliffs stood at $850 per short ton. Meanwhile, HRC prices currently stand at $826 per short ton. Both Nucor and Cliffs cited increased “market transparency” as the rationale for the moves. Nucor stated its published pricing aimed to reduce market volatility and they did not intend it to replace other HRC indexes.

A few takeaways:

- It remains safe to assume that Nucor and Cliffs do and will continue to operate in their own best interest. While both companies stated that their weekly published pricing would benefit customers, the mills likely hope to influence HRC indexes at the very least.

- Nucor’s first published price ($825 per short ton) stood at the bottom of the market. Opening at a lower cost was likely part of a plan to boost the credibility of its newly published steel prices. However, this could shift over time as establishing an inflated market floor would benefit domestic mills.

- Increased control over domestic prices may indeed help reduce volatility, which has been apparent over recent years. However, it is worth noting that Nucor’s decision came immediately following a nearly 26% quarterly decline in steel prices as mills lost control of the price trend. This suggests that mills appear primarily concerned with steel price volatility to the downside.

- Other major domestic producers, particularly SDI and U.S. Steel, declined to publish their own prices. However, this will allow both to fall in line with Nucor and Cliffs without risking the legal implications of price fixing.

- It remains unclear to what extent negotiations will impact the prices buyers pay. Historically, larger buyers have greater bargaining power. Nonetheless, the ability of mills to influence market conditions will continue to require them to manage the supply-demand balance through capacity discipline.

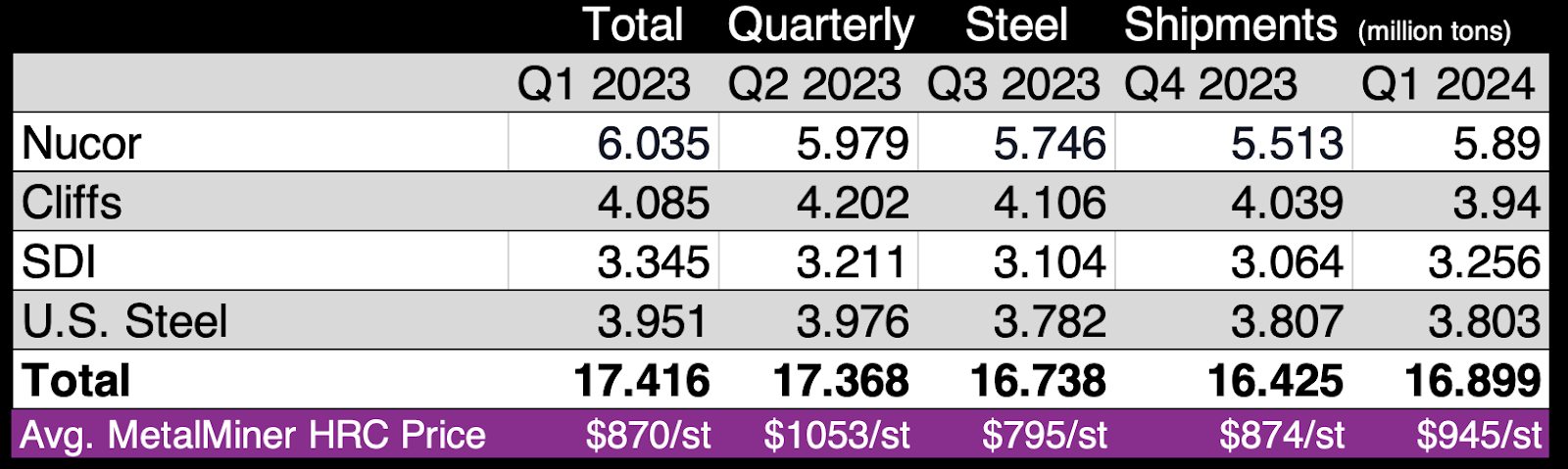

Mill Quarterly Reports Show Mixed Results

Q1 2024 saw mixed results among steel mills with steel prices. Overall, shipments from the four leading domestic producers trended up from the previous quarter. Both Nucor and SDI saw an increase in total shipments, which offset quarterly declines from both U.S. Steel and Cleveland-Cliffs.

Historically, Q1 typically sees an uptick in steel shipments, so the increase is unsurprising. However, shipments fell across all mills from Q1 2023. This suggests weaker conditions on an annual basis. Despite the nearly 3% decrease in shipments from Q1 2023 to Q1 2024, the average Q1 MetalMiner HRC price rose 8.62% year over year.

Source: MetalMiner Insights,

Risks Mount for Nippon’s U.S. Steel Acquisition

The future of U.S. Steel remains in limbo as election-year politics continue to see Nippon’s potential acquisition draw ire from both sides of the aisle. Once the crown jewel of American manufacturing, U.S. Steel shrunk from its place as the world’s largest steel producer and corporation. By 2022, U.S. Steel’s position fell to the 24th-largest steel producer following years of underperformance.

Trump promised to block the sale if elected, while President Biden vowed to keep U.S. Steel a “totally American company.” Although there is no guarantee that either candidate will fulfill their campaign promises, the mill remains a bargaining chip that could derail Nippon’s plans.

Recently, the U.S. Department of Justice opened an antitrust investigation into the takeover. By early May, the ongoing investigation triggered Nippon to delay the closing of the acquisition despite approval from U.S. Steel’s shareholders. The company now expects closing to occur in December, after previous expectations that it would be complete by September. However, this new timeline would push the deal beyond November’s presidential election.

Cliffs CEO Lourenco Goncalves Fires Shots at Nippon Steel

After losing the initial bidding war for U.S. Steel, Cliffs remains interested should the deal fall apart. In fact, Cliffs CEO Lourenco Goncalves continues to critique the sale. During the steelmaker’s Q1 earnings call, the outspoken CEO stated, “It still baffles me to this day that the clueless individuals representing Nippon Steel in this embarrassing event felt that they could do this without union support.” He noted later that the White House “has different ways to terminate the Nippon transaction, and we believe that will be done sooner rather than later.”

The sale’s blockage would seemingly guarantee a domestic buyer. This would increase mill consolidation in the U.S., which has historically given domestic producers greater control over prices. The ongoing challenges could also cause Nippon to look for a U.S. partner in the deal, although this remains merely speculative.

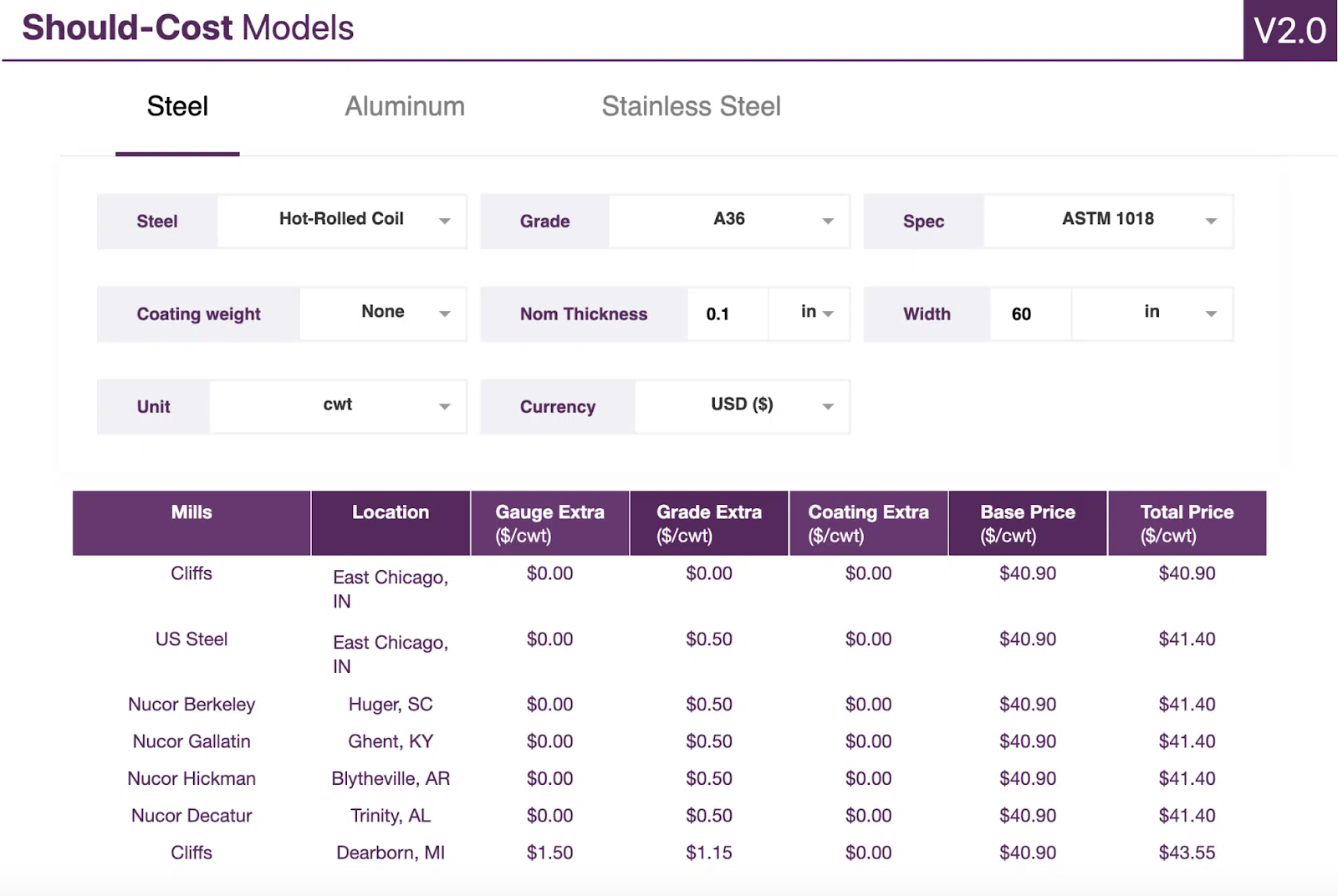

Want to know more about changing steel prices? MetalMiner should-cost models give your organization levers to pull for more price transparency from service centers, producers and part suppliers. Explore the models now.

By Nichole Bastin

More Top Reads From Oilprice.com:

- Russia’s Oil Revenues Doubled in April Compared to a Year Earlier

- Biden Administration Bans Fossil Fuels in Federal Buildings

- U.S. Continues to Tighten Grip on Russia's Military and Industrial Sectors