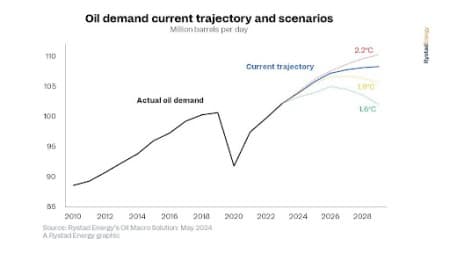

Oil demand will rise further in the medium term, according to Rystad Energy research and modeling, as low-carbon alternatives are not yet sufficiently developed or economically competitive to offset the growing demand for transportation and industrial services. Rystad Energy’s latest Oil Macro Scenarios report explains how the 13 sectors that rely on oil will face a more complex transition than expected just a couple of years ago. These findings underscore the notion that oil demand remains sticky and the process of substituting the capital stock associated with oil consumption will be complex and lengthy due to the competitive advantages of oil in multiple transportation sectors and industrial processes.

The research evaluates the five-year demand trajectory of oil, the technological readiness of each sector to transition and the policy frameworks supporting that shift. Our analysis sheds light on the impact of crucial breakthroughs, such as the rapid electrification of buses, rail and cars, as well as the challenges faced by the remaining sectors that lack fully developed or competitive alternative technologies.

As oil demand is likely to stay on an upward trajectory in the medium term, the probability of a fast transition away from oil decreases unless we witness breakthroughs in those low-carbon energy carriers that can technically and economically substitute oil. Our updated mid-term forecast should bring a dose of realism to the oil transition narrative, alongside a renewed sense of urgency to explore and invest even more – wherever it makes economic sense – in clean tech and renewables, to achieve those breakthroughs.

Claudio Galimberti, Global Market Analysis Director, Rystad Energy

Transportation

About a quarter of global oil demand comes from passenger road transportation, so it is no surprise that the adoption of electric vehicles (EVs), which comprise both battery electric vehicles (BEV) and plug-in-hybrid (PHEV), is a key factor to estimate the oil demand impact. EVs have risen since 2018, making up 16% of global sales in 2022. However, last year saw an inflection point – with global EV sales landing only at 19% – due to a combination of lack of mass-market EVs outside of China, poor charging infrastructure, low consumer acceptance in some regions, charging insecurity, and the withdrawal of subsidies in some countries. Related: Memorial Day Travel Expected to Near Record High

Despite these challenges, Rystad Energy still predicts that the electrification of passenger road transport will regain force in the second half of this decade and beyond. Car manufacturers have committed to producing tens of millions of EVs in the coming years, which will bring about economies of scale. Still, it is important to note that some of these plans have recently been scaled back due to poor returns on investment. In the end, one big problem will need to be solved: the “charging insecurity” in areas where car owners do not own private parking spots. This phenomenon is particularly acute in many non-OECD countries and in quite a few OECD ones as well.

Beyond passenger road transport, the transition to alternative energy sources faces headwinds. In heavy-duty commercial road transport, oil demand is expected to grow in line with the expansion of the global economy, especially in Asia, as alternatives to oil remain limited. As an example, batteries are still too heavy and large to fit in a Class 8 truck and, even if they did, it would take too long to charge them. Battery swapping, a process where batteries with low charge get replaced with fully charged ones at specialized stations, has shown promise in China, but it is still a tiny fraction of the electric truck fleet. Catenary and induction charging – methods of charging electric vehicles while they are in motion – could be a solution, but they are currently too expensive. Granted, Volvo and Tesla have started the production and delivery of electric semitrucks, but the numbers are still small and will continue to be so in the medium term.

The maritime industry shares many of the same challenges as heavy-duty trucks. Shipping large cargo across the seas efficiently and affordably requires a fuel with high energy density, safe storage and transport and a well-established supply chain. While alternatives like ammonia and methanol may satisfy some of these requirements, they are yet to outcompete oil on key metrics like affordability and energy density. Furthermore, the fast aging of the global maritime fleet is set to slow down the fleet turnover.

Sustainable Aviation Fuel (SAF) is an environmentally friendly alternative to traditional jet fuel. Although SAF has the potential to grow significantly in the aviation industry during the 2030s and beyond, it will not significantly impact aviation in the next five years. Despite major commitments from airlines and the International Civil Aviation Organization's (ICAO) Corsia program, SAF's share will be less than 5% of jet fuel demand by the end of this decade. This translates to less than 0.4% of global oil demand.

Buses and rail transportation don't have to wait for alternatives as they are already available and proving to be highly effective. The recent electrification trend in these two sectors in China, India and Europe will continue in the coming years, thanks to government policies. However, even if these two sectors were to be fully electrified in the next 15 years, the maximum reduction in oil demand by 2030 would only be around 0.5-0.8 million barres per day since they currently represent less than 3% of oil demand.

Stationary sectors

The stationary sectors, which include petrochemical, industry, building, non-energy use, energy own use, power and agriculture, account for 42.3% of global oil demand as of 2024 and are vital components of the energy transition. In the petrochemical sector, demand for plastics is set to surge in the coming years – on the back of an expanding global middle class – and oil and natural gas liquids (NGLs) will be the feedstock used to produce plastic. To reduce demand for virgin feedstock, mechanical and chemical recycling rates must increase. However, higher investment in the recycling supply chain, as well as research and development, are needed to achieve this. It is important to recall that global plastic recycling rates are currently only 8% of total plastic consumption, with scant evidence that they could increase significantly by the end of the decade.

Oil demand in the building sector has proven more resilient than expected just a few years ago. In regions where the natural gas grid is not available and winters are long and frigid, oil – in the form of liquified petroleum gas (LPG), kerosene or gasoil – remains the most efficient energy carrier for space and water heating. Heat-pumps, which are typically very efficient for space heating in milder climates, tend to have a reduced effectiveness in very cold regions. Finally, in countries that still rely on burning biomass for cooking, such as sub-Saharan Africa, LPG could be a cleaner energy carrier, which could result in a 1.5 million barrels per day (bpd) uptick in oil consumption.

High energy density is essential in the industry sector to achieve the high temperatures required for operations such as steelmaking, cement production, petrochemicals, and refining subsectors. Although hydrogen is considered the most viable low-carbon energy carrier alternative to oil, it is unlikely to become a strong competitor in the next five years due to high costs and lack of a developed supply chain.

Our research confirms that oil demand remains sticky and it will take time and resources to switch the capital stock associated with its consumption. It also reminds us of the importance of understanding the whole energy system end-to-end, and not just the oil system. Lowering global emissions is still possible in the medium term if other energy sectors deploy clean technology and renewables at a faster pace. In this context, the rapid deployment of solar PV in power generation, displacing coal, has done just that over the past few years. As a result, a fast reduction in global emissions is still within reach, despite climbing oil demand.

By Rystad Energy

More Top Reads From Oilprice.com:

- Oil Prices Climb on a U.S. Inventory Draw and Inflation Optimism

- Memorial Day Travel Expected to Near Record High

- The IEA Has Cut Its Oil Demand Growth Forecast for 2024

Even without Its research, it has always been known that the biggest drivers of global oil demand are transportation followed by petrochemicals and plastics. This state of affairs isn’t going to change well into the future.

The rationale is that EVs are a fad and therefore will never ever prevail over ICEs.

Moreover, the global demand for petrochemicals is on the rise underpinned by crude oil producers wanting to add value to their exports and the increasing need for petrochemicals. The same logic applies to plastics particularly recyclable ones.

Hopes by both the IEA and Rystad Energy to sea peak oil demand reached before 2030 with rising demand for EVs are no more than pipe dreams and wishful thinking.

Dr Mamdouh G Salameh

International Oil Economist

Global Energy Expert